Real Client Scenarios: Credit Repair Wins From Bakersfield

Five real situations from Bakersfield clients we’ve worked with since 2016. Names changed for privacy. The strategy is real.

Numbers on a credit report aren’t just numbers — they’re whether you can buy a house, drive a reliable car, or sleep through the night without worrying about a collector calling. Here are five real situations from Bakersfield clients we’ve worked with since 2016. Your story might look a lot like one of these.

The First-Time Homebuyer in Northwest Bakersfield

- Disputed both medical collections under FCRA §611 with debt validation letters under FDCPA §809

- Both collectors failed to validate within 30 days → both deleted

- Sent a goodwill letter to the auto lender citing two years of perfect payments since the late

- Auto late removed as a goodwill courtesy

Mid-FICO climbed to 651 within 70 days. Closed on a 3-bedroom in Northwest Bakersfield three months later.

The Single Mom Recovering From Identity Theft

- Filed identity theft affidavit with the FTC at IdentityTheft.gov

- Used the affidavit to file FCRA §605B blocked-reporting demands with all three bureaus

- Filed a police report with Bakersfield PD

- Frozen credit at all three bureaus

All five fraudulent items removed within 45 days. Score climbed from 542 to 689 once the legitimate accounts were the only thing showing.

The Construction Worker With Old Charge-Offs

- Pulled Metro 2 data and identified Date of First Delinquency errors on both charge-offs (re-aged)

- Submitted FCRA §623 disputes directly with the furnishers, citing Metro 2 non-compliance

- Negotiated pay-for-delete on the open collection — paid 40% in exchange for written deletion agreement

Both charge-offs deleted (re-aging violation). Open collection deleted after PFD. Score rose to 671 in 90 days.

The Couple With High Credit Card Utilization

- Built an AZEO payoff plan over 60 days

- Coordinated payment timing to statement closing dates

- Requested credit limit increases on three seasoned cards (no hard pulls)

Husband’s score 612 → 718. Wife’s score 624 → 732. No disputes filed — pure utilization strategy.

The Senior on Fixed Income Facing a Garnishment

- Reviewed the underlying debt — collector could not produce chain of title

- Helped client prepare a pro se Notice of Opposition to Claim of Exemption in Kern County Superior Court

- Sent FDCPA §809 validation demand to the debt buyer

- Filed FCRA dispute citing the unverified judgment

Garnishment opposition led to settlement at 25% of original demand. Judgment vacated by stipulation. Tradeline deleted. Score rose to 643.

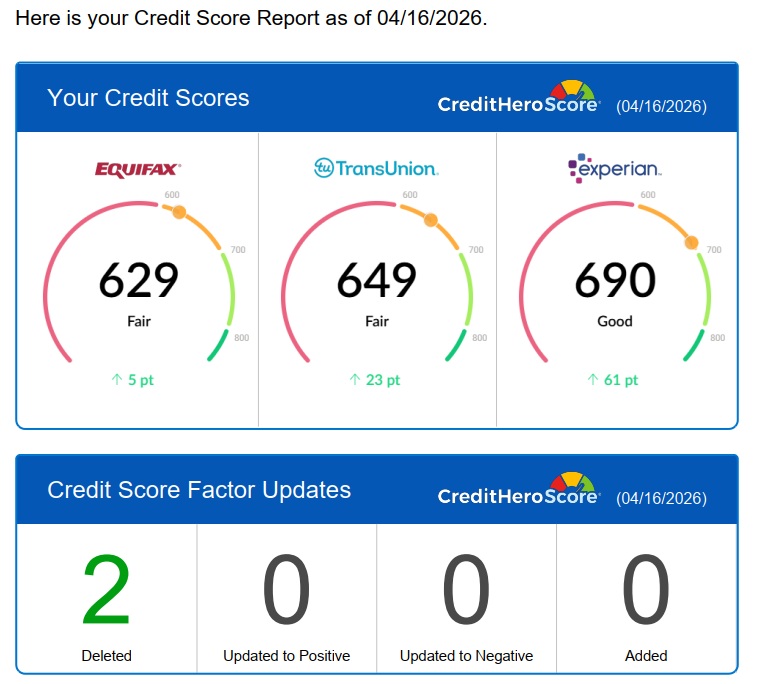

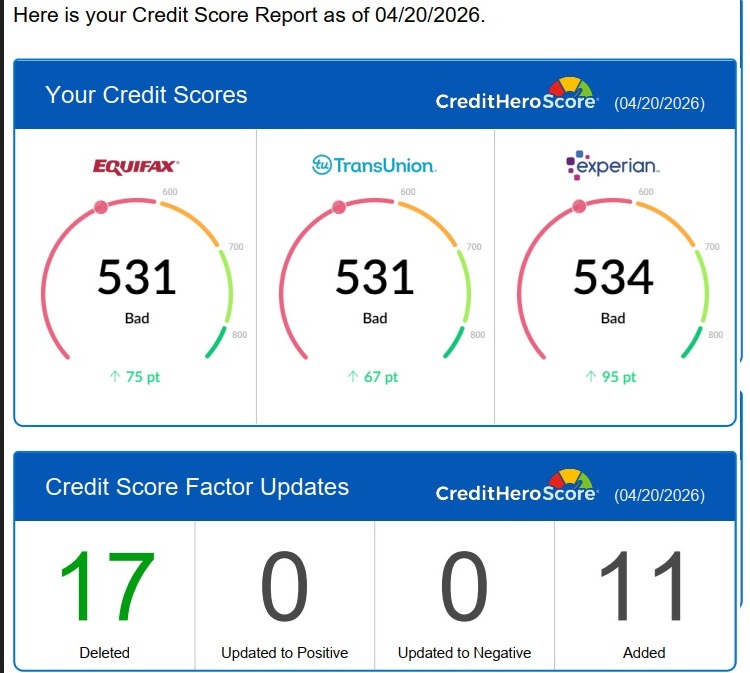

Real Score Results — Before & After

These are actual screenshots from two recent Bakersfield clients. All personally identifying information has been redacted. Used with written client permission.

Score Climbed Significantly in 30–60 Days

Timeframe: 30–60 Days

Major Score Improvement in 30–90 Days

Timeframe: 30–90 Days

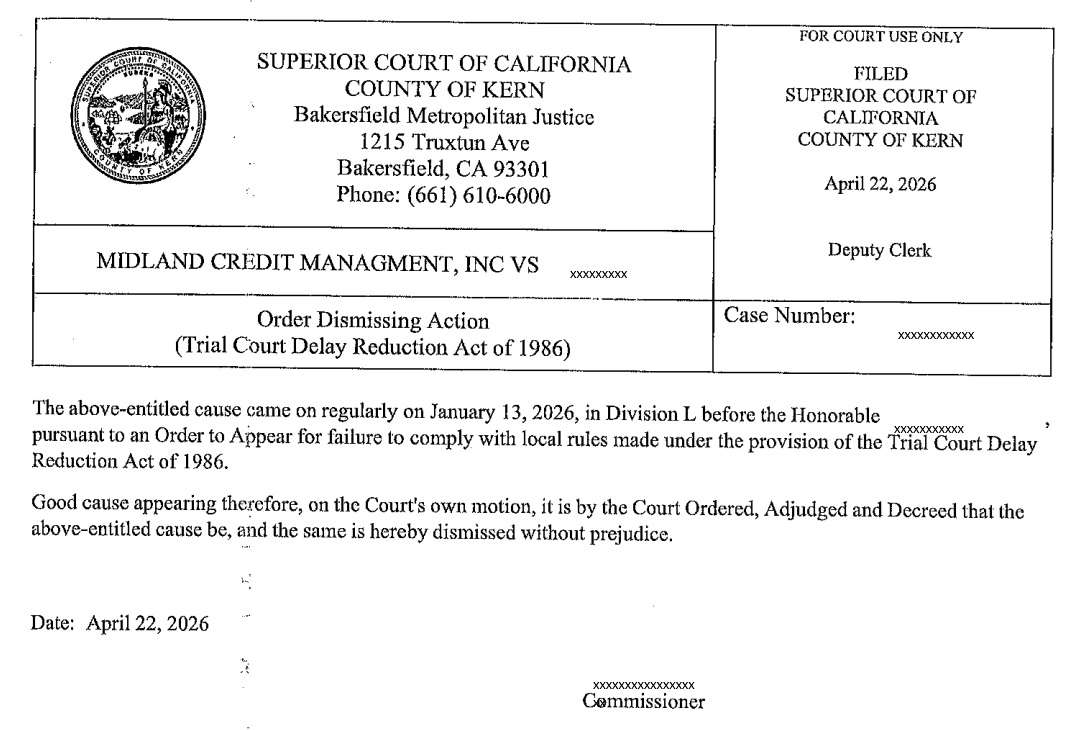

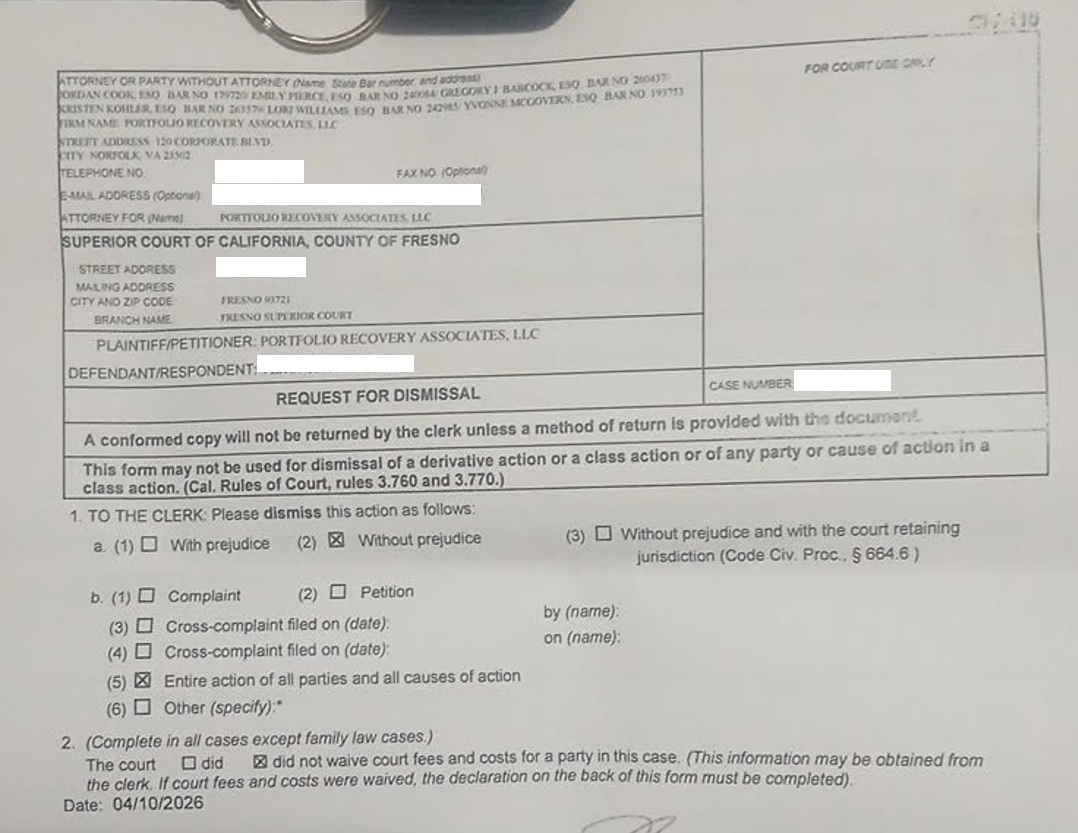

When Lawsuits Get Dismissed

Some clients come to us already being sued by creditors or third-party debt buyers. Here are two recent cases where the lawsuits were dismissed within months of the client engaging our consumer-protection support services.

⚖️ Important Legal Notice — Please Read

Maximum FICO Score is not a law firm and does not provide legal advice or legal representation. The dismissals shown below were the outcome of legal proceedings, not the result of credit repair services alone.

Our role with these clients was to provide consumer-protection support — including FDCPA §809 debt validation demands, document organization, and education about FCRA, FDCPA, and Rosenthal Act consumer rights. Clients made their own legal decisions and, where appropriate, were referred to or worked with licensed California attorneys.

If you are facing a lawsuit, judgment, or wage garnishment, you should consult with a licensed California attorney. The State Bar of California Lawyer Referral Service can be reached at calbar.ca.gov.

Creditor Lawsuit Dismissed

This client came to us after being served with a debt collection lawsuit from a third-party debt buyer. Through documented FDCPA §809 validation demands, the underlying debt could not be verified. The client worked with a California-licensed attorney for the court process, and the case was dismissed.

Debt Collector Case Dismissed

Another Bakersfield client served with a collection lawsuit from a junk-debt buyer. After validation demands and a coordinated legal response, the case was dismissed. The associated negative tradelines were also disputed under FCRA §611 and removed from the credit report.

Some clients leave reviews after their lawsuits are dismissed. Some after they hit their target score. Some just because the process felt different than what they expected. Here are their words.

What Bakersfield Says About Us

Very helpful people and they listen to your concerns. Thanks to Isaac and staff.

Excellent customer service. Quick to respond and always available for guidance.

I had a couple of collections affecting my credit score so I went to Isaac for some guidance on getting things sorted out and he was very knowledgeable and passionate about his work. He helped me from start to finish and went beyond my expectations and I’m very grateful for what he and his team did for me. I would recommend him to anyone that’s in need of financial and credit guidance — it’s not easy doing it alone and good help isn’t easy to find nowadays. Thank you Isaac and the team at Maximum FICO Score!

Isaac Palacios has done everything he has told me he could do regarding my account and after several months I’ve finally received 710+ score! Never thought it was possible with the accounts and history I’ve made at such a young age!

What These Stories Have in Common

Every one of these wins came from the same playbook:

- Pull all three reports — never work from one bureau

- Identify the actual violation — Metro 2, FCRA, FDCPA, or all three

- Cite the exact law in every dispute letter

- Track every deadline — bureaus are bound by 30-day timers

- Combine strategies — utilization fixes plus disputes plus goodwill

There’s no magic. There’s just law, leverage, and patience.

Frequently Asked Questions

Are these results typical?

Results vary based on the items on your report, the responsiveness of furnishers, and your own credit habits. We make no guarantees — that would violate CROA. We do guarantee a 90-day money-back policy if we don’t perform.

How long does most credit repair take?

Most Bakersfield clients see meaningful score increases within 60 to 120 days. Complete cleanups can take 6 to 9 months depending on complexity.

Do you work with people who have bankruptcies?

Yes. Discharged bankruptcies stay on your report for 7 (Chapter 13) to 10 (Chapter 7) years, but the individual accounts included in the bankruptcy must be reported correctly. Errors on those tradelines are very common and disputable.

Can you really remove old collections?

Sometimes — when they’re inaccurate, unverifiable, or non-Metro-2-compliant. We never promise a specific deletion. We promise to fight for it within the law.

Your Story Could Be Next

If any of these scenarios sound like you, get a free assessment. We’ll pull your reports, find the violations, and tell you honestly what we can and can’t do.

Get Your Free Assessment Call (661) 505-8085These real-world credit repair scenarios demonstrate that meaningful score improvements are achievable with the right strategy. First, understanding which negative items are disputable under the FCRA is essential. Furthermore, each situation requires a tailored approach — for example, a client with a repossession needs a different strategy than one with medical collections. Additionally, working with a BBB A+ accredited firm like Maximum FICO Score ensures that all dispute work is done in a CROA-compliant manner. As a result, clients avoid common pitfalls and see faster, more reliable results.

However, the timeline varies: some clients see changes within 30–45 days, while others require several months of consistent effort. In contrast to DIY credit repair, professional guidance helps clients prioritize the items most likely to yield score gains. Overall, these case studies show that with patience and the right expertise, substantial credit improvement is within reach for most consumers. If you see yourself in any of these scenarios, consider scheduling a free credit analysis with our Bakersfield team.

Real client results vary, but common outcomes include: removal of inaccurate collection accounts, correction of payment history errors, improved utilization through coaching, and score increases that qualify clients for mortgage loans, auto financing, or rental housing they could not previously access.

Most clients working with Maximum FICO Score see initial improvements (item deletions or corrections) within the first 30–60 days. More complex situations with multiple collections or serious derogatory items typically take 3–12 months to achieve meaningful score improvements.

Maximum FICO Score serves Bakersfield and Kern County clients dealing with collections, late payments, charge-offs, identity theft errors, medical debt, student loan issues, and more. Many clients are preparing to buy a home, start a business, or improve their overall financial position.

Yes. Many mortgage denials are due to specific credit score or credit report issues that can be addressed. After credit repair, clients are often able to qualify for an FHA or conventional mortgage within 6–18 months. Coordinating with a local lender and credit repair specialist together maximizes results.

Yes, but it takes time. FHA requires a minimum 3-year waiting period after foreclosure (less with extenuating circumstances). During that time, rebuilding credit through secured cards, on-time payments, and reducing debt sets the stage for qualification. With diligent effort, reaching the required 580–620 minimum is achievable.