Last updated: May 15, 2026

A complete, federally compliant playbook for raising your FICO credit score — built on what FICO actually measures.

Your FICO credit score affects almost every financial decision you make — the interest rate on your mortgage, whether you qualify for an auto loan, what credit cards you can open, even how much you pay for insurance in some states. The good news: FICO publishes exactly how the score is calculated, and the strategies that move it are knowable and federally protected.

Quick Answer

FICO scores are calculated from five factors: payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%). The fastest-moving factor is utilization — paying down balances before your statement closing date can show results within one billing cycle. Results vary by credit file. No service can guarantee specific score outcomes under CROA.

This guide is the practical playbook. It walks you through what FICO actually measures, the specific strategies that move each factor, the federal rights that protect you when negative information is wrong, and the common mistakes that quietly hold scores back. Results depend on your individual credit file, but the principles below are the same ones used by every consumer who has built strong credit.

What Your FICO Score Actually Measures

A FICO score is a three-digit number between 300 and 850 that estimates how likely you are to repay borrowed money on time. Lenders use it to decide whether to approve you and at what interest rate. The standard FICO tiers:

FICO Score Tiers

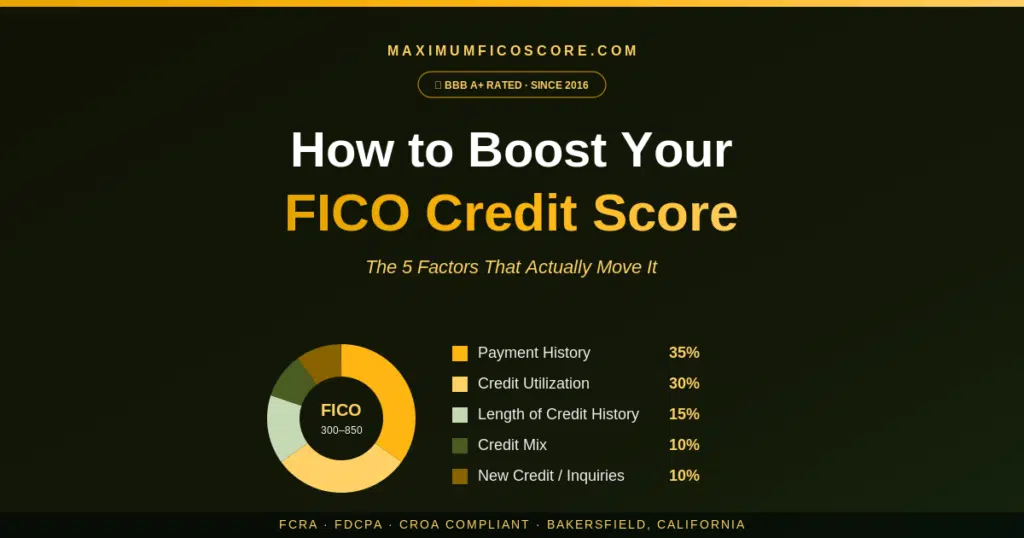

Fair Isaac Corporation (the original FICO) publishes the five factors used in the calculation and their approximate weightings:

How FICO Calculates Your Score

Two factors — payment history and credit utilization — together control 65% of your score. If you only focus on those two, you control nearly two-thirds of what FICO measures. The other three factors matter, but they refine the picture once the big two are dialed in.

Strategy 1: Payment History (35%)

Payment history is the single most important factor in your FICO score. The model rewards consistent on-time payments and penalizes late payments, collections, charge-offs, and other adverse events. To boost your score, this section needs to be as close to perfect as possible going forward.

What FICO is measuring:

- Whether each scheduled payment was made on time

- How late any missed payments were (30, 60, 90, 120+ days)

- How recently the late payments occurred

- How many accounts have late payments

- Public records like bankruptcies, judgments, and tax liens

What to do: Set up automatic minimum payments on every revolving account you have. Even paying the minimum on time is far better than a missed payment. A single 30-day late payment can drop a strong credit score by 60–110 points and stay on your report for up to seven years under the Fair Credit Reporting Act (FCRA § 605, 15 U.S.C. § 1681c).

If you have late payments that are inaccurate — payments you actually made on time, accounts that weren’t yours, or wrong dates — you have the right to dispute them. See how to remove negative items from your credit report for the full FCRA dispute process.

Strategy 2: Credit Utilization (30%)

Credit utilization is the ratio of your current revolving balances to your total available credit limits. If you have a $10,000 credit limit and you’re carrying a $3,000 balance, your utilization is 30%. This is the fastest-moving factor in your FICO score — changes here can show up within a single billing cycle.

The general guidance:

- Under 30%: Acceptable — won’t actively hurt you

- Under 10%: Strong — supports higher scores

- Under 5%: What top-tier consumers typically maintain

- 1–3% with at least one card reporting a small balance: Often cited as optimal

Credit Utilization Target Zones

What to do: Pay down balances before your statement closing date, not just before the due date. Credit card issuers report your balance to the credit bureaus once per month — usually on the statement closing date. If you pay the balance down before that date, the low balance is what FICO sees.

FICO looks at both total utilization across all cards and per-card utilization. Maxing out one card while keeping others at zero hurts your score more than spreading the same total balance evenly across multiple cards. Aim for low utilization on every individual card.

Your Rights Under Federal Law

If Inaccurate Items Are Holding Your Score Down

No credit improvement strategy works if your credit report contains errors. The Fair Credit Reporting Act (15 U.S.C. § 1681) gives you specific rights to challenge anything that’s inaccurate, incomplete, or unverifiable:

- The right to free credit reports from each bureau at AnnualCreditReport.com

- The right to dispute any item (§ 611) — bureaus have 30 days to investigate

- The right to have items deleted if they can’t be verified

- The right to dispute directly with furnishers (§ 623)

- The right to sue for willful violations — $100–$1,000 statutory damages per violation (§ 1681n)

You can exercise every one of these rights yourself, at no cost, without hiring a credit repair company. They are yours by federal law.

Strategy 3: Length of Credit History (15%)

FICO measures the age of your credit history as a combination of three numbers: the age of your oldest account, the age of your newest account, and the average age of all accounts on your file. Older histories generally support higher scores.

What to do: Don’t close your oldest credit cards unless they carry annual fees you can’t justify. A 10- or 15-year-old account anchors your average age substantially — closing it can drop your average age by years overnight, which can lower your score.

If a card has no annual fee and you don’t use it actively, keep it open and put one small recurring charge on it (like a streaming subscription) that auto-pays in full each month. That keeps the card active in the issuer’s eyes and keeps the account reporting positive payment history.

Strategy 4: Credit Mix (10%)

FICO rewards consumers who have successfully managed different types of credit:

- Revolving credit: Credit cards, retail cards, lines of credit

- Installment credit: Mortgages, auto loans, personal loans, student loans

What to do: Don’t open new accounts just to diversify your mix — the temporary inquiry hit and the interest costs almost always outweigh the small score benefit. But if you naturally need credit (you’re financing a car or a home), having both revolving and installment accounts on your file does help.

Strategy 5: New Credit and Inquiries (10%)

Every time you apply for new credit, the lender pulls your credit report. This is a hard inquiry. Hard inquiries stay on your report for two years and affect your score for the first 12 months.

Hard vs. Soft Inquiries

Rate-shopping bonus: Multiple mortgage or auto loan inquiries within 14–45 days count as ONE inquiry under modern FICO models.

What to do: Apply for new credit only when you actually need it. A single new credit application might drop your score by 5–10 points temporarily. Applying for three new cards in a month signals risk and costs more.

Quick Wins You Can Act on This Week

If you’re reading this and want to do something today, here are five high-impact actions that take less than an hour total:

- Pull your three free credit reports from AnnualCreditReport.com. This is the only federally authorized source. Don’t pay for them anywhere else.

- Set up autopay on every revolving account. Even paying just the minimum prevents missed payments — the single biggest risk to your score.

- Pay down your highest-utilization card to under 30% before its next statement closing date. The change can show up on your next credit report.

- Make a list of any items on your reports that look wrong — accounts you don’t recognize, wrong dates, late payments you remember making on time, balances that don’t match your records.

- Don’t apply for new credit until you’ve gotten the rest of your file in shape.

Common Mistakes That Quietly Hurt Your Score

“Carrying a small balance helps build credit.” False. Carrying any balance month-to-month just means paying interest. Pay your statement in full every month. The bureau still sees that you used the card and paid it.

“Closing old cards I don’t use cleans up my credit.” Usually false. Closing an old card reduces your total available credit (raising your utilization ratio) and reduces your average account age. Both hurt your score.

“Checking my credit hurts my score.” False. Pulling your own report is a soft inquiry. Check it as often as you want.

“Paying off a collection account removes it.” Usually false. Paying a collection often updates its status to “paid” but doesn’t delete it from your report. The account can remain for up to seven years from the original delinquency date.

“Income is part of my credit score.” False. Your income is not used in any FICO scoring model. Lenders consider income when deciding to approve you, but it doesn’t enter into the score itself.

How Long Does It Take to See Real Results?

Realistic Timeline of Credit Score Changes

This depends entirely on your starting point and your specific credit file. Credit utilization changes can show up within one billing cycle. New positive payment history builds gradually. Negative items naturally fade in impact over time but stay on your report for up to seven years under the FCRA.

For a detailed breakdown of what realistically affects your timeline — and what no service can legally promise — read our companion guide: how long does credit score improvement really take?

If you’re targeting the elite tier specifically, we also have a dedicated guide: how to reach an 800+ FICO credit score.

Common Questions

What’s the fastest way to boost my FICO score?

For most consumers, lowering credit utilization is the fastest lever. Paying revolving balances down to under 10% before the statement closing date can produce a meaningful score change in the next billing cycle. Disputing inaccurate negative items under the FCRA can also produce fast results if the items can’t be verified by the bureau within 30 days.

Should I pay off my credit cards in full or carry a balance?

Always pay your statement in full when you can. There is no FICO benefit to carrying a balance — that’s a long-running myth. Carrying a balance just means paying interest. The bureau sees your activity from the statement itself, not from whether you carried debt.

Will paying off old collections improve my score?

It depends on which FICO scoring model your lender uses. Newer models (FICO 9 and 10) ignore paid collections entirely. Older models still in widespread use treat paid collections more favorably than unpaid ones but don’t fully erase the impact. If a collection is inaccurate or unverifiable, disputing it under the FCRA is the better path.

How many credit cards should I have?

FICO doesn’t penalize you for having multiple cards as long as you use them responsibly. Consumers with the highest scores typically have 3–6 credit cards, all paid in full each month, with low overall utilization. Don’t open new cards just to hit a number — only when you genuinely need additional credit.

Can I improve my score without paying for credit repair?

Yes. Every right credit repair organizations use to improve credit reports is available to you directly under the FCRA, at no cost. What credit repair companies add is time savings, paperwork management, and escalation experience. Whether that’s worth paying for depends on your time, the complexity of your file, and your comfort with the dispute process.

Does checking my own credit hurt my score?

No. Pulling your own credit is a soft inquiry. You can check it as often as you want with no impact on your score. Many credit card issuers provide free FICO scores monthly.

Take the Next Step

Get a Professional Review of Your Credit File

Want an honest, written assessment of what’s actually moving your score? Our team will review your three-bureau credit report at no cost — no pressure, no obligation.

Book Free Credit AssessmentOr call Client Support (661) 505-8085

About the Author

Isaac Palacios is the founder of Maximum Fico Score, a BBB A+ rated credit repair and credit education company based in Bakersfield, CA, serving clients across all 50 states since 2016. Maximum Fico Score operates in full compliance with the Fair Credit Reporting Act (FCRA), the Fair Debt Collection Practices Act (FDCPA), and the Credit Repair Organizations Act (CROA). For credit consultation: Client Support (661) 505-8085.

Disclaimer: This article is for educational purposes only and does not constitute legal or financial advice. Under the Credit Repair Organizations Act, we cannot and do not guarantee any specific credit score increase or the removal of any specific item from a credit report. Individual results vary based on the accuracy of items reported and factors specific to each credit file. Consumers have the right to dispute inaccurate information directly with the credit reporting agencies free of charge.

Obtain your reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Review each account for inaccurate balances, incorrect payment history, accounts that are not yours, or outdated items past 7 years. File disputes with the bureaus reporting each error online or by certified mail with supporting documentation.

The most damaging errors are: inaccurate late payment notations (directly affects 35% of your score), accounts that are not yours (could include high balances or negative history), incorrect account status (showing delinquent when it should be current), and balances reported higher than the actual amount.

Once a dispute is resolved and the bureau corrects or removes the item, your score updates within days to a few weeks. Most consumers see the updated score within 1–2 billing cycles after the correction. The score impact depends on how significant the removed or corrected item was.

This is called reinsertion, which is regulated by the FCRA. The bureau must notify you within 5 days of reinserting a deleted item and provide contact information for the furnisher. You can dispute again with documentation of the previous removal. Repeated wrongful reinsertion may support a legal claim.

Yes, in some industries. Many employers in financial services, government, law enforcement, and certain professional sectors run credit checks as part of background screening. Inaccurate negative items on your report could unfairly harm your employment prospects — another strong reason to keep your report error-free.