The AZEO Method: How to Optimize Credit Utilization and Maximize Your FICO® Score

Maximum FICO Score • Credit & FICO Education • Bakersfield, CA

If you’ve been researching how to raise your score quickly before a mortgage, auto loan, or refinance, you’ve probably run into four letters: AZEO. It stands for All Zero Except One, and it’s one of the most effective — and most misunderstood — ways to optimize the credit utilization portion of your FICO score. This guide explains exactly what it is, why it works, and how to execute it safely, step by step.

What the AZEO Method Actually Is

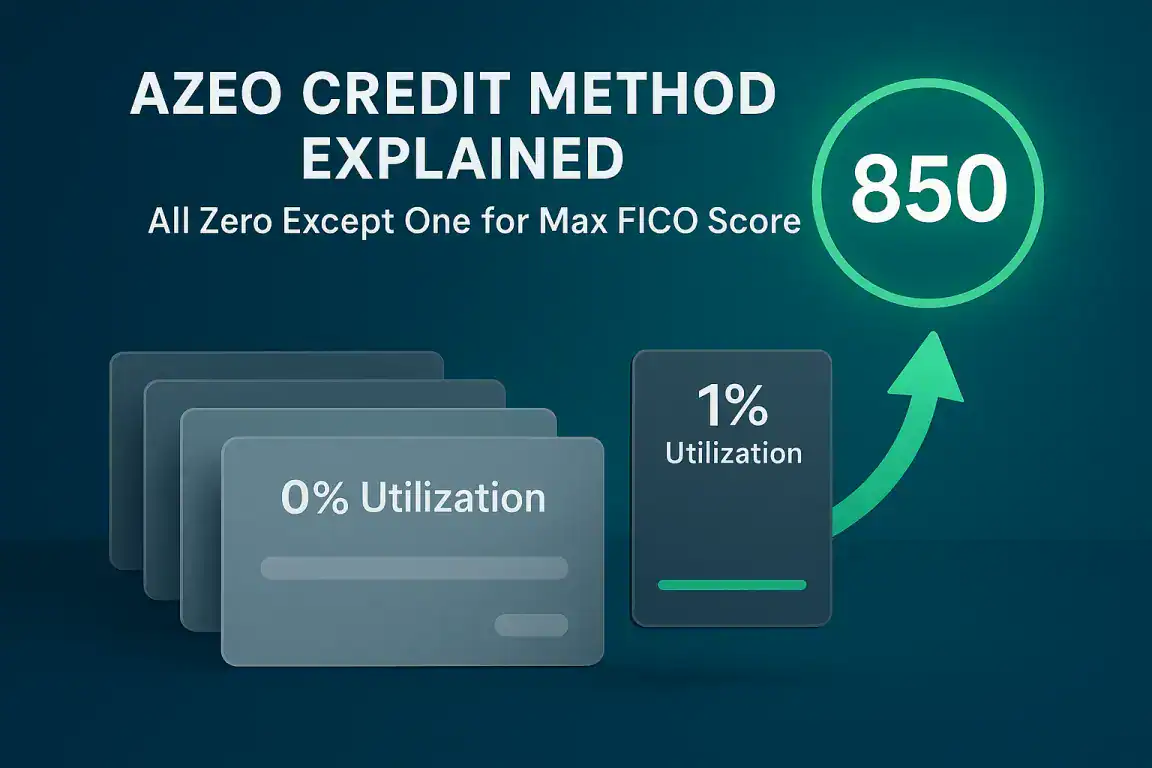

AZEO — All Zero Except One — is a credit-card balance strategy. The idea is simple: you pay down every revolving credit card to a $0 reported balance except for one card, which you allow to report a small balance (typically 1–9% of that card’s limit). When the credit bureaus take their monthly snapshot, your profile shows almost no debt — but still shows active, healthy card usage. Here’s the key insight most people miss: your FICO score doesn’t look at what you owe today. It looks at the balance each card reports on its statement closing date. AZEO is about controlling that reported number — the snapshot — rather than how you spend day to day.Why AZEO Works: Utilization and Your FICO Score

Credit utilization — the percentage of your available revolving credit you’re using — is one of the most powerful factors in the FICO scoring model, accounting for roughly 30% of your score. It’s second only to payment history, and unlike payment history, it can change dramatically from one month to the next. That makes it the fastest lever most consumers can pull. FICO actually measures utilization two ways, and AZEO is designed to optimize both at the same time:- Aggregate (overall) utilization — your total reported balances across all cards divided by your total credit limits. AZEO drives this close to zero.

- Per-card (individual) utilization — the balance on each single card versus that card’s own limit. AZEO keeps every card at 0% except one card sitting in the low single digits.

The percentages that matter

- Under 30%: acceptable — the minimum most lenders want to see.

- Under 10%: strong — where meaningful score gains typically appear.

- 1–9% on one card, 0% on all others: the AZEO target — optimized for both aggregate and per-card utilization.

- 0% on everything: good, but often slightly less effective than leaving one small balance.

How to Execute AZEO Safely, Step by Step

The most important thing to understand is timing. Because your score reacts to reported balances, you have to pay your cards down before each card’s statement closing date — not the due date. The closing date is when the balance is captured and sent to Experian, Equifax, and TransUnion. Here’s the process we walk Bakersfield credit repair clients through:- Find each card’s statement closing date. It’s on your statement or in your online account — and it’s usually about three weeks before your payment due date. Write down the closing date for every card.

- Choose your “one” card. Pick a single card — ideally one of your older accounts or one with a mid-range limit — to carry the small reported balance.

- Pay the other cards to zero before their closing dates. A few days before each card closes, pay the balance down to $0 so it reports zero. Leaving it a day or two early gives the payment time to post.

- Leave a small balance on your one card. Aim for a reported balance of roughly 1–9% of that card’s limit (for a $1,000 limit, that’s $10–$90). Don’t pay it to zero before it closes — let the small balance report.

- Pay the statement in full by the due date. After the balance reports, pay that remaining balance off by the due date so you never carry debt or pay interest. AZEO is a reporting strategy, not a reason to revolve a balance.

- Repeat each cycle before you apply. Utilization has no memory — it resets every month. Run AZEO for the statement cycle (or two) right before you apply for a mortgage, auto loan, or new credit, when the optimized snapshot matters most.

Common AZEO Mistakes to Avoid

AZEO is safe and legitimate — it’s just careful timing of your own money. But small errors undo the benefit. Watch for these:- Paying by the due date instead of the closing date. This is the #1 mistake. Pay by the due date and your high balance has usually already reported. Always work to the closing date.

- Closing old cards to “simplify.” Closing a card removes its limit from your total available credit, which raises your utilization and can shorten your average account age. Keep old accounts open.

- Letting all cards report $0. Leave one small balance so your profile still shows active revolving use.

- Opening a new card right before applying. The hard inquiry and lower average account age can offset your utilization gains at the worst possible time.

- Carrying the balance and paying interest. AZEO never requires you to revolve debt. Let the small balance report, then pay it in full.

- Forgetting business or charge cards. Know which of your cards report to the personal bureaus and which don’t, so you optimize the right accounts.

What AZEO Can’t Fix — and What Can

Here’s the honest part. AZEO is powerful for one specific thing: optimizing your current utilization so your score reflects your best possible snapshot. But it can’t touch the other things that may be quietly holding your score down — a collection that isn’t yours, a late payment reported in error, a charge-off with the wrong balance, or a duplicate account inflating your debt. Utilization tricks can’t remove inaccurate history; only a proper review and dispute under the Fair Credit Reporting Act (FCRA) can address those. That’s the difference between optimizing a score and correcting a credit report. AZEO handles the first. If you suspect inaccurate, outdated, or unverifiable items are dragging you down, the next step is a professional audit of all three of your reports. As a BBB A+ rated credit repair Bakersfield team, that’s exactly what we do — and your first look is free.Claim Your Free Credit Audit

See exactly what’s helping and hurting your score across Experian, Equifax, and TransUnion. No obligation, no pressure — just an honest, FCRA-compliant review from our Bakersfield credit repair team. Claim Your Free Credit Audit Prefer to talk first? Book Your Free Consultation →This article is educational only and does not constitute legal or financial advice. AZEO is a personal credit-management strategy; results vary by individual credit profile, and no specific score increase is guaranteed. Maximum FICO Score is a credit repair organization operating in full compliance with the Fair Credit Reporting Act (FCRA), the Fair Debt Collection Practices Act (FDCPA), and the Credit Repair Organizations Act (CROA). Consumers have the right to dispute inaccurate information directly with the credit reporting agencies free of charge. © 2016–2026 Maximum Fico Score, Bakersfield, CA.