Step-by-step instructions, FCRA compliance guide, and free dispute letter template.

If you see something on your credit report that looks wrong — a late payment you didn’t make, an account you don’t recognize, a balance that’s incorrect, or outdated information — you have a federal right to challenge it using the FCRA dispute process. Specifically, the Fair Credit Reporting Act (FCRA) Section 611 guarantees your right to dispute any inaccurate, incomplete, or unverifiable information on your credit report.

This guide walks you through your rights, explains what you can and cannot effectively dispute, and provides step-by-step instructions for filing disputes with credit bureaus and creditors directly. Importantly, disputing costs nothing and does not hurt your credit score.

Under FCRA §611, you have the federal right to dispute any inaccurate, incomplete, or unverifiable item on your credit report. File a dispute with the credit bureau in writing (certified mail recommended). They have 30 days to investigate; 45 days if you provide additional information during the investigation. Additionally, written notification of the outcome is required by law. If they verify the item but you still disagree, you can add a 100-word consumer statement, file a CFPB complaint, or consult an FCRA attorney. Disputing does not hurt your score.

Key Takeaways

- Under FCRA §611, you have the right to dispute any inaccurate, incomplete, or unverifiable item on your credit report.

- Credit bureaus must investigate within 30 days (45 days if you provide additional info).

- You can dispute online, by phone, or by mail — certified mail is recommended for a paper trail.

- You can dispute directly with the creditor under FCRA §623.

- Disputing does NOT lower your credit score.

- If the bureau “verifies” an inaccurate item, you can add a consumer statement, file CFPB/FTC complaints, or pursue legal action.

- Credit repair companies can dispute on your behalf under CROA (Credit Repair Organizations Act) — no advance fees allowed.

Your Legal Right to Dispute (FCRA §611)

Specifically, the Fair Credit Reporting Act (15 U.S.C. §1681i) gives you the right to dispute any information in your credit report that you believe is inaccurate, incomplete, or unverifiable. Moreover, this is a federal consumer protection law that applies to all credit bureaus and creditors — not just one.

The Bureau’s Investigation Obligation

When you file a dispute, the credit bureau must:

- Investigate your dispute within 30 days (or 45 days if you provide additional information during the investigation).

- Contact the creditor (called the “furnisher”) and ask them to verify or correct the information.

- Delete or correct any information that cannot be verified.

- Notify you in writing of the outcome.

- Provide a free copy of your updated credit report if the dispute results in a change.

15 U.S.C. § 1681i — Fair Credit Reporting Act, Section 611. This law requires bureaus to maintain “maximum possible accuracy” in your file. See also § 1681s-2 (Data Furnisher Obligations) — creditors must ensure accuracy when reporting.

What You Can and Cannot Dispute

Not all items are equally effective to dispute. However, understanding the difference between what works and what doesn’t will save you time and protect your strategy. For collections specifically, see our complete guide to removing collections from your credit report — disputes are one of several tools.

You CAN Effectively Dispute:

- Wrong payment status. Shows late, but you paid on time. Bank records prove payment.

- Accounts you don’t recognize. Identity theft, fraud, or reporting errors.

- Duplicate accounts. Same account reported twice on your report.

- Wrong balance or credit limit. Shows incorrect amount owed or available credit.

- Outdated information past the 7-year reporting window. Items older than 7 years (10 for bankruptcy) should be removed.

- Medical collections that violate 2022–2023 bureau rules. See our medical debt rules guide — paid medical collections and all medical collections under $500 must be removed.

- Accounts from identity theft. File a police report and dispute with proof.

- Wrong personal information. Incorrect name, address, Social Security number.

You CANNOT Effectively Dispute:

- Accurate late payments. When a payment was genuinely late, the bureau will verify it as accurate with the creditor’s records.

- Legitimate collections. A valid collection account will be verified by the debt collector and will remain on your file — unless you negotiate a pay-for-delete letter with the collector directly.

- Real charge-offs. Charged-off accounts stay on your report for 7 years — though you can still dispute any inaccurate balances or dates within the entry.

- Real bankruptcies. These cannot be removed early and must naturally age off after 10 years.

- Accurate delinquencies. Any negative item that is factually accurate will be verified and retained by the bureau.

Focus disputes on items you have evidence to challenge — wrong dates, incorrect balances, accounts not opened by you, or information past the 7-year window. Therefore, these have the highest success rates. Advanced disputers also look for Metro 2 violations — formatting errors in how creditors report data — which can force deletion even of accurate items. Do not dispute items you know are accurate without a Metro 2 angle; otherwise, the bureau will verify them and mark your dispute as “frivolous,” which can delay future disputes.

3 Ways to File a Dispute

1. Online at Bureau Websites (Fastest, No Paper Trail)

Visit the bureau’s website and use their online dispute form:

- Equifax.com — Dispute Center

- Experian.com — Dispute Center

- TransUnion.com — Dispute Center

Pro: Fastest response. Con: No proof you filed; harder to show you disputed if issues arise.

2. By Certified Mail (Recommended — Creates Legal Paper Trail)

Instead, send a dispute letter to the bureau’s dispute address via USPS Certified Mail with Return Receipt Requested. Keep copies of everything.

Pro: Best legal protection; proof of delivery; documented timeline. Con: Takes 2-3 days to mail and receive.

3. By Phone (Quickest, Weakest Option)

Alternatively, call the bureau’s customer service line. Get a dispute reference number and always follow up in writing.

Pro: Immediate filing. Con: No paper trail; disputes may not be documented if you don’t follow up in writing.

Use certified mail as your primary method. Include copies (not originals) of supporting documentation. Keep the certified mail receipt and return receipt. As a result, this creates an indisputable record of your dispute and the bureau’s 30-day deadline for response.

Step-by-Step: How to Write a Dispute Letter

A clear, professional dispute letter is your best tool. As a result, taking time to write it correctly gives you the strongest possible legal foundation for your dispute.

Sample Dispute Letter Template

[Your Name]

[Your Address]

[City, State ZIP]

[Your Phone]

[Your Email]

Date: [Today’s Date]

To: [Bureau Name — Choose One]

Equifax, P.O. Box 740241, Atlanta, GA 30374

Experian, P.O. Box 4500, Allen, TX 75013

TransUnion, P.O. Box 2000, Chester, PA 19022

RE: Dispute of Inaccurate Information Under FCRA §611

Dear Sir or Madam,

I am writing to dispute inaccurate information on my credit report. Under the Fair Credit Reporting Act (15 U.S.C. § 1681i), I have the right to challenge any information that is inaccurate, incomplete, or unverifiable. I request that you investigate the following item(s) and remove or correct them accordingly.

MY INFORMATION:

Name: [Full Name]

Social Security Number: XXX-XX-[Last 4 digits]

Date of Birth: [MM/DD/YYYY]

ACCOUNT IN DISPUTE:

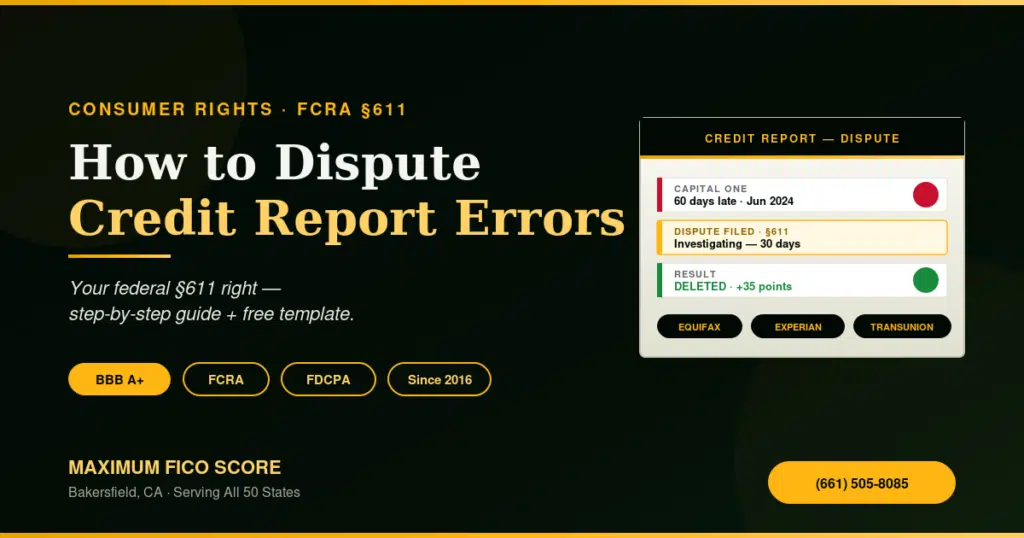

Creditor: [Account Name — e.g., Capital One]

Account Number: [Last 4 digits only — XXXX9999]

Account Status: [e.g., Shows 60-day late]

Reported Balance: [Amount]

REASON FOR DISPUTE:

This account is inaccurate because [state the specific error — e.g., “it shows 60 days late, but my bank records prove I paid this account on time in June 2024”]. I have never been delinquent on this account.

SUPPORTING DOCUMENTATION:

Enclosed are copies of [bank statement, payment confirmation, etc.] that prove [payment made, account paid off, etc.].

I request that you remove this inaccurate item from my credit report and notify all three major credit bureaus of the correction. Under FCRA §611, you must complete your investigation within 30 days (or 45 days if I provide additional information). Please notify me in writing of the results.

Thank you for your prompt attention to this matter.

Sincerely,

[Your Signature]

[Your Typed Name]

Documentation and Mailing Requirements

Send copies (not originals) of: bank statements proving payment, cancelled checks, settlement letters, correction letters from creditors, or any documentation supporting your claim. Include a brief cover letter listing what you’re enclosing. Do NOT send originals; bureaus don’t always return them.

Disputing Directly With the Creditor (FCRA §623)

Notably, you don’t have to dispute only with the bureau. In fact, under FCRA §623, you can dispute directly with the original creditor (the “data furnisher”). This approach is often faster and can be equally effective, particularly when the creditor has the most direct access to payment records.

How Creditor Disputes Work

- Timeframe: Creditors have 30 days to investigate and respond (same as bureaus).

- Outcome: If they confirm the error, they must update all three bureaus within 15 days.

- Best for: Recently paid collections, closed accounts showing as open, paid charge-offs still showing balance.

- Often faster: Creditors usually have more direct access to account records than bureaus do during their investigation.

Real-World Example: Creditor Dispute

A Bakersfield consumer notices a Capital One account reporting 60 days late in June 2024. Fortunately, they have bank records showing the payment cleared on time. After sending a dispute letter directly to Capital One’s dispute department with copies of the bank statement, Capital One reviews their internal records, confirms the payment was processed correctly, and notifies all three bureaus that the late payment was reported in error. As a result, both Equifax and Experian remove the late payment — and the consumer’s score improves.

What Happens After You File a Dispute?

The Timeline (30-45 Days)

- Days 1-3: Bureau receives your dispute and opens an investigation file.

- Days 4-20: Bureau sends your dispute to the creditor (furnisher) and requests verification of the account.

- Days 21-30: Creditor responds to bureau with verification or correction. Bureau updates your file based on creditor’s response.

- Day 30-45: Bureau notifies you in writing of the outcome and provides your updated credit report (free, if changes were made).

Possible Outcomes

| Outcome | What It Means |

|---|---|

| Deleted | Item completely removed from your report (best outcome). |

| Updated/Corrected | Item corrected (e.g., late payment removed, balance corrected). |

| Verified Accurate | Bureau found the item is accurate; it stays on your report. |

| Not Verified | Creditor didn’t respond; item must be removed within 5 business days. |

If the Bureau Says “Verified” but You Know It’s Wrong

Fortunately, you have several escalation paths available:

- Add a Consumer Statement (100 words max): Request to add a statement to your file explaining your dispute. For example: “I dispute this late payment — I have proof of timely payment in my bank records.” This has limited score impact, but it documents your disagreement on the record.

- File a CFPB Complaint: Go to consumerfinance.gov/complaint and submit a complaint against the bureau or creditor. The CFPB investigates these cases and their responses are officially documented.

- Submit an FTC Report: Go to ftc.gov/complaint to report the inaccuracy and any improper verification. This creates a federal record of the issue.

- Try Pay-for-Delete: If the item is a collection that the bureau verified as accurate, you can still negotiate removal directly with the collector. Our pay-for-delete letter guide walks through the full 5-step process and includes a free template.

- Consult an FCRA Attorney: Under 15 U.S.C. §1681p, you can sue for statutory damages up to $1,000 plus actual damages and attorney fees if a bureau willfully fails to comply with FCRA requirements.

What to Do Next After Your Dispute Resolves

Once the investigation closes, pull an updated copy of your credit report to confirm the change was applied correctly. Consequently, if a deletion occurred, allow one billing cycle for your FICO score to reflect the update. In addition, if you disputed the same item with multiple bureaus, verify the outcome on all three — corrections on one bureau do not automatically apply to the others.

Real-World Example: Successful Dispute in Bakersfield

A Bakersfield resident noticed a Synchrony Bank credit card on their report showing a 60-day late payment in May 2024. They had actually settled the account in April 2024 and had the settlement letter. They sent a certified dispute letter to all three bureaus with a copy of the settlement letter. Equifax and TransUnion removed the late payment within 30 days. Experian verified it. The consumer then sent a dispute directly to Synchrony Bank (data furnisher) with the settlement letter and bank statement showing the settlement was paid. Synchrony confirmed the account was paid in full and notified Experian. Experian updated the account to “settled” and removed the 60-day late. The consumer’s score improved by 35 points.

Results vary based on individual credit profiles and documentation. This is a hypothetical example for educational purposes.

Keeping Records and Following Up

Create a Dispute Tracking Log

In order to stay organized throughout the entire process, keep a simple spreadsheet that captures:

- Date dispute filed

- Bureau (Equifax, Experian, TransUnion)

- Account/creditor name

- Dispute reference number (if provided)

- Expected response date (30-45 days)

- Outcome (deleted, verified, updated)

- Certified mail receipt number

- Follow-up notes

What to Save

- Original dispute letter (signed copy)

- Copies of supporting documents (bank statements, settlement letters, etc.)

- Certified mail receipt (shows you mailed it)

- Return receipt (shows bureau received it)

- Bureau’s written response to your dispute

- Updated credit report showing changes

- Any follow-up correspondence

When to Follow Up

Meanwhile, if you don’t hear back by day 35, call or email the bureau and ask about your dispute status. Be sure to reference your certified mail receipt number. In cases where they have no record of your dispute, you will therefore need to refile and confirm certified mail delivery before proceeding further.

Frequently Asked Questions

Questions About Timelines and Additional Options

Ready to Dispute Inaccurate Items?

Maximum FICO Score specializes in identifying disputable items on your credit report and handling the dispute process on your behalf — FCRA compliant, no upfront fees, transparent throughout.

About Maximum FICO Score

Maximum FICO Score is an ethical, CROA-compliant credit repair company serving Bakersfield, Kern County, and clients nationwide. Our team specializes in identifying disputable negative items, disputing on your behalf, and helping you exercise your consumer rights under the FCRA and FDCPA.

Founded in 2016, our approach is built on transparency and education first. Rather than making false promises, our company never charges upfront fees and never guarantees specific results. Every client receives a 3-day cancellation right and full clarity on what disputes can reasonably accomplish.

Address: 4646 Wilson Road, Suite 101, Bakersfield, CA 93309

Client Support: 661-505-8085

Email: support@maximumficoscore.com

Website: maximumficoscore.com

Key Takeaways: Disputing Your Credit Report

First, understanding your rights under the Fair Credit Reporting Act is the essential starting point for any successful credit dispute. Furthermore, Section 611 of the FCRA legally requires credit bureaus to investigate disputed items within 30 days and correct or delete unverifiable information. Additionally, data furnishers — the companies that report your account information — are equally responsible for investigating disputes and correcting inaccurate data they reported. However, simply submitting a dispute letter without supporting documentation often results in a quick but unsatisfying “verified” response from the bureaus. In contrast, disputes accompanied by specific evidence — statements, police reports, or creditor correspondence — are far more likely to result in a correction or deletion.

Consequently, keeping a detailed paper trail of every dispute, including certified mail receipts and bureau responses, is critical if you need to escalate to a regulatory complaint or legal action. As a result, consumers who document their disputes thoroughly and follow up consistently tend to achieve better and faster outcomes. Overall, the dispute process — while sometimes lengthy — is one of the most powerful consumer rights tools available at no cost. Specifically, Maximum FICO Score helps Bakersfield clients craft targeted, legally sound dispute strategies that maximize the likelihood of successful corrections. Similarly, our bilingual team ensures that every Spanish-speaking client understands their dispute rights and the full process from start to finish.

Disclaimer: This content is for educational purposes only and does not constitute legal or credit repair advice. Maximum FICO Score does not guarantee the removal of items from your credit report or specific credit score improvements. Results depend on individual credit profiles and supporting documentation. Consult a qualified FCRA attorney for legal advice specific to your situation.

Legal References: Fair Credit Reporting Act (FCRA): 15 U.S.C. § 1681 (§609 right to access, §611 dispute rights, §623 data furnisher obligations, §616 consumer statement). Credit Repair Organizations Act (CROA): 15 U.S.C. § 1679. Fair Debt Collection Practices Act (FDCPA): 15 U.S.C. § 1692.

First, document the specific error with your account statements or other evidence. Then file a dispute online, by certified mail, or by phone with the bureau(s) reporting the error. Each bureau must investigate within 30 days and notify you of the outcome. If the item is inaccurate, they must correct or remove it.

You can dispute any information on your credit report that you believe is inaccurate, incomplete, or unverifiable. This includes wrong account balances, incorrect payment history, accounts that are not yours, outdated information, and identity errors. You cannot dispute information simply because you do not like it or it is accurate.

Strong dispute evidence includes: bank statements showing on-time payments, letters from creditors confirming account status, correspondence showing account settlement or payoff, identity theft reports from the FTC, court documents, and written communication from the creditor confirming an error.

If your dispute is verified and the item remains unchanged, you can add a 100-word consumer statement explaining your dispute. You can also file a complaint with the CFPB, escalate the dispute with new evidence, or consult an FCRA attorney about potential legal remedies.

File an identity theft report at IdentityTheft.gov (FTC website), then use that report when disputing accounts with the bureaus. With an FTC identity theft report, bureaus are required to block fraudulent information. Also place fraud alerts or a credit freeze to prevent additional fraudulent accounts.